The S&P 500 has risen by 10.7% over the past two weeks, reaching a new all-time high. The last comparable episode dates back to March 2000, at the peak of the dot-com bubble. At that time, the market was also posting rapid gains amid already elevated valuations. The following decade proved disappointing for investors. Today’s situation raises similar questions. The rally is not driven by undervalued assets, but is occurring while valuation multiples are already high. Historically, however, it is the starting level of valuations that determines long-term performance.

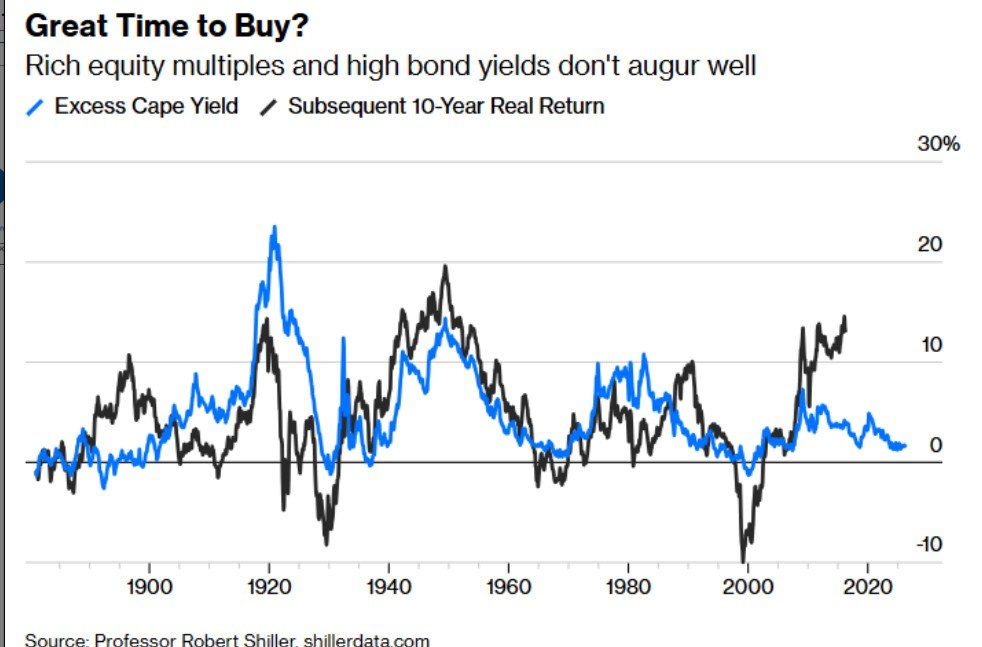

Economist Robert Shiller introduced the CAPE (cyclically adjusted price-to-earnings) ratio, which smooths corporate earnings over a full cycle to estimate the market’s “true” value. His concept of Excess CAPE Yield has, for more than a century, been one of the most reliable indicators of future returns. The higher valuations are today, the lower expected returns tend to be tomorrow and vice versa. Shiller’s research shows a strong inverse relationship between current valuation multiples and real returns over a ten-year horizon. When valuations reach extremes, as in 1929, 2000, or partly in the 2020s, the following decade almost inevitably delivers weak results.

Today, we once again find ourselves in a zone where this signal is becoming concerning. The Excess CAPE Yield is at low levels, which historically has meant limited upside potential and elevated risks of correction. At the same time, the market appears to be overlooking significant constraints, including high interest rates, elevated debt levels, and slowing global growth.